19 minute read

There has been a lot of momentum over the last couple of years as regulators across the globe are moving to put more structure and definition around business in the financial services industry who manage assets in line with ESG/ sustainability principles.

Just as asset managers are hindered by a lack of data and disclosure from the companies they are looking to potentially invest in, so too are the asset owners, and the intermediaries who support them, challenged by a lack of consistency and disclosure on ESG managed products from asset managers.

This section gives an overview of the key regulation and guidance that has been recently introduced, or is soon to be implemented, in Europe. This is a rapidly evolving space and we will endeavor to keep this section up to date as developments emerge. This version is up to date as of June 2021.

European regulation

Europe is the most advanced region globally both in terms of demand for sustainable and ESG products and therefore unsurprisingly in terms of regulation and legislation aimed at managers who provide such products.

As much of this regulation is coming into effect after the UK has formally left the EU, it will not automatically be on-boarded into UK law. However, as the UK Government has been vocal about their desire to ‘lead from the front’ on ESG, the general expectation is that the UK will introduce similar legislation to their EU counterparts. The EU legislation will directly apply to UK firms who market to EU investors or manage EU funds or products. Firms who are not directly required to follow the legislation may still choose to do so in order to stay abreast of their peers and not suffer reputationally.1

UK Sustainable Disclosure Regulation

Following Brexit, the UK government and the FCA have made clear that they with the UK to be a global leader on sustainable and responsible investing. Many commentators therefore anticipate the FCA’s landmark regulation, the SDR to go above and beyond Europe’s SFDR. This regulation closed for consultation in January 2023 with final the final rules set to be published in the first half of the year.

In October 2022, the FCA unveiled three new categories of investment labels to be used for sustainable investment products:

Sustainable focus: products investing in assets that are environmentally or socially sustainable

Sustainable improvers: products investing in assets to improve environmental or social sustainability over time

Sustainable impact: products investing in solutions to environmental or social problem targeting measurable impact.

The new requirements will also restrict how terms such as ESG, green or sustainable can be used in product names /and marketing, and require firms to make consumer-facing disclosures to explain the key sustainability-related features of a product.2

EU Taxonomy

Read: MacFarlanes – EU Taxonomy Regulation Overview

Read: MacFarlanes – EU Taxonomy Regulation Overview

Key points:

- The taxonomy establishes the terminology and toolkit for assessing whether economic activities are considered sustainable

- The aim is to enable investors to more effectively compare ‘environmentally sustainable’ funds, and reduce greenwashing

- A fund is deemed ‘environmentally sustainable’ if the portfolio meets four conditions:

- ‘contributes sustainably’ to one of more environmental objectives, or enables other activities to make a sustainable contribution

- Does not ‘significantly harm’ (DNSH) any of the environmental objectives

- Is invested in compliance with the Taxonomy regulation minimum safeguards

- Complies with technical screening criteria established by the Commission (when published)

- Environmental objectives:

- Climate change mitigation

- Climate change adaptation

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

- Financial products that have sustainable objectives (Article 9 products) are required from Jan 2022 to disclose:

- Information on the environmental characteristics to which the underlying investments contribute

- A description of how/ to what extent the underlying investments are made in economic activities that qualify as ‘environmentally sustainable’

- What proportion of investments are ‘environmentally sustainable’

The EU Sustainable Finance Disclosure Regulation – SFDR

Regulation (EU) 2019/2088 on sustainability-related disclosures in the financial services sector (i.e. the Disclosure Regulation, ESG Regulation or SFDR), is part of a broader legislative package under the European Commission’s Sustainable Finance Action Plan.

Under SFDR funds and mandates are classified into three categories: Articles 6, 8 and 9.

- Article 6: funds which do not integrate any kind of sustainability into the investment process and could include stocks currently excluded by ESG funds such as tobacco companies or thermal coal producers

- Article 8 ‘environmental and socially promoting’: ‘where a financial product promotes, among other characteristics, environmental or social characteristics, or a combination of those characteristics, provided that the companies in which the investments are made follow good governance practices’

- Article 9 ‘products targeting sustainable investments’: products targeting bespoke sustainable investments, ‘where a financial product has sustainable investment as its objective and an index has been designated as a reference benchmark’

Read: MacFarlanes – EU Disclosure Regulation Overview

Key points:

- SFDR requires firms to make strategic business and policy decisions regarding their approach to ESG which must be disclosed on the firm’s website and in pre-contractual and periodic disclosure

- Focus of the regulation is on the provisions of information to investors (asset managers), clients (asset owners) and other stakeholders

- In order to meet the disclosure requirements, many firms are likely to require significant system and control changes, as well as significant allocation of resources

- The disclosure applies at the firm and all product level, not just those with an ESG focus

- Given the uncertainty around how EU legislation may be on-shored in the UK following at the end of the Brexit transition period – UK based firms can either take a ‘wait and see’ approach or voluntarily adopt the regulation

- UK firms who market to EU investors, as well as those with EU funds or mandates, will have to comply with the regulation

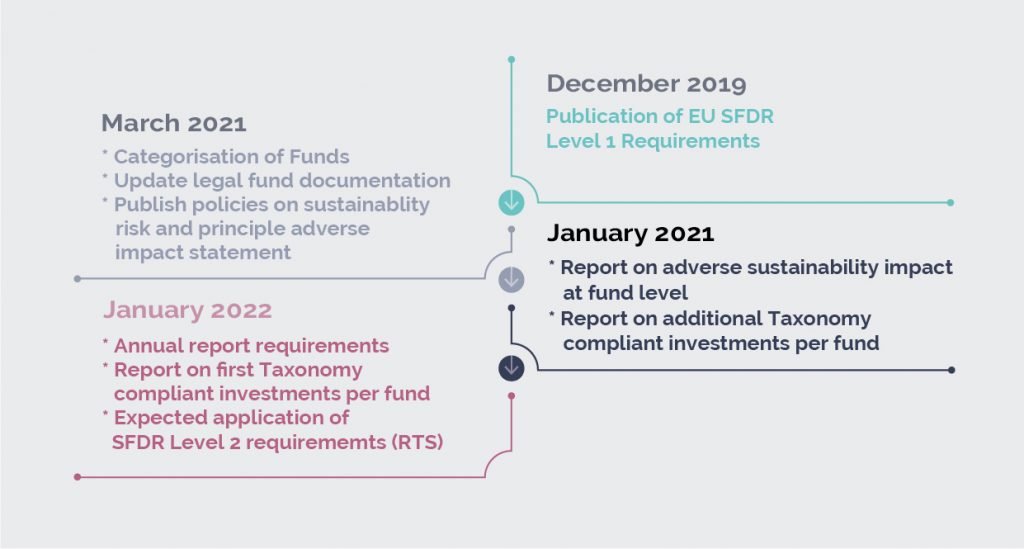

- The majority of legislation that relates to the firm came into effect in March 2021, with the second stage set to be implemented in December 2022 that relates to product level disclosures on principal adverse impacts

Recommended Read: MacFarlanes – Brexit and the Disclosure Regulation

SFDR timeline

Upcoming European regulation: Regulatory Technical Standards – RTS (SFDR Level 2)

Read: Simmons & Simmons – Top ten things asset managers need to know about the level 2 proposals under the SFDR pages 2-8

Key points:

- Currently still in draft form, the RTS proposes the detail on the disclosure requirements that were first laid out under Level 1 of SFDR.

- The details are significantly more onerous than had been expected by the industry and would represent a very significant undertaking for in-scope firms.

- The UK Government has indicated that the finalised RTS will not be automatically on-shored into UK law, but has provided no indication whether the UK Level 2 provisions may diverge or will be an effective copy-out.

- The SFDR, and the RTS, applies to the defined concept of financial market participant, or FMP. The definition of FMP includes:

- MiFID firms providing the service of portfolio management

- AIFMs

- UCITS managers

- A sub-set of rules also apply to financial advisers

- The draft RTS sets out granular specifications for the content, methodology and presentation of certain disclosures, covering:

- Entity-level ‘adverse impact’ website disclosures – details of the asset manager’s policy for assessing the adverse impacts of its investment decisions/recommendations on sustainability factors

- Product-level disclosure for ESG focussed products – pre-contractual, website and periodic disclosures relating to Article 8 and Article 9 products

- SFDR Article 4 required asset managers with over 500 employees to include a statement on their website communicating their policies for monitoring the adverse impacts of their investment decision on sustainability factors

- The draft RTS proposes that this description includes a KPI grid comprising up to 50 separate quantitative disclosures on complex ESG metrics (see note appendix for full detail)

- Managers will be required to disclose on:

- All 32 mandatory metrics

- At least 1 indicator on adverse climate/ environmental impacts

- At least one metric on social/ employee/ human rights/ anti-corruption/ anti-bribery impacts

- Any other impacts qualifying as principle (no guidance has been given yet as to how to define whether an impact qualifies as ‘principle’)

- Managers will be required to disclose on:

- The purpose of the quantitative disclosure is to provide a comparable measure of the adverse impacts of a given asset manager’s investments

- Managers are likely to face significant challenges to collect the data needed to meet the required disclosures. The RTS suggests methods such as:

- Direct engagement with investee companies

- Internal financial analysis

- External market research providers

- Specifically commissioned studies

- Publicly available information

- Shared information from peer networks or collaborative initiatives

- The narrative/ qualitative disclosure required within the adverse sustainability impacts statement include:

- Description of policies to identify and prioritise principal adverse sustainability impacts

- Description of actions to address principal adverse sustainability impacts

- Description of engagement policies and their efficacy

- Reference to adherence of international standards

- As well as an overarching narrative summary of the qualitative and quantitative disclosures

- The main aim of product specific pre-contractual disclosures is to prevent greenwashing by providing information on the characteristics of the product that will not mislead investors

- The draft RTS suggests that information will be disclosed using mandatory templates

- The draft RTS provides more detail to supplement the SFDR requirement for managers of Article 9 or 8 products to publish and maintain sustainability disclosure information on their website – these are less prescriptive than the requirements for pre-contractual and periodic disclosures as there are no required templates

- The focus of periodic disclosures is on the success of a product in attaining its environmental/ social characteristics or sustainable investment objective. The draft RTS introduces the requirement to use a mandatory reporting template

Further European Commission legislative and regulatory updates – April 2021

Read: Norton Rose Fulbright –European Commission adopts legislative and regulatory package on sustainable finance

Key points:

In April 2021 the European Commission published a number of legislative and regulatory initiatives with the Sustainable Finance Action Plan (2018), including:

- A Delegated Regulation under Regulation (EU) 2020/852 on the establishment of a framework to facilitate sustainable investment (Taxonomy Regulation) establishing the technical screening criteria for economic activities qualifying as contributing substantially to climate change mitigation or climate change adaptation;

- A proposal for a Corporate Sustainability Reporting Directive (CSRD);

- Six amending Delegated Acts incorporating sustainability issues and considerations into the EU financial services regulatory framework

Delegated Regulation laying down technical screening criteria for economic activities qualifying as contributing substantially to climate change mitigation or climate change adaptation

- The EU Taxonomy Climate Delegated Act sets out the technical screening criteria for the first two environmental objectives – climate change mitigation and climate change adaptation – as well as the application of the ‘do no significant harm’ (DNSH) criteria

- The Climate Delegated Act contains the technical screening criteria setting out the conditions under which a wide range of economic activities qualify as contributing substantially to climate change mitigation or climate change adaptation, and for determining whether those economic activities do no significant harm to one or more of the other environmental objectives

Proposal for a Corporate Sustainability Reporting Directive (CSRD)

- Amends the existing reporting requirements under the Non-Financial Reporting Directive

- Scope is expanded to include large listed and non-listed companies and listed Small and Medium-Sized Enterprises, and will require an audit (assurance) of reported sustainability information

- New rules will introduce more detailed non-financial reporting requirements as well as a requirement to report according to mandatory EU sustainability reporting standards

- The proposal includes an obligation for companies to digitally ‘tag’ the reported information to make it machine-readable

Delegated Acts incorporating sustainability issues and considerations into the EU financial services regulatory framework

- Level 2 measures seek to incorporate sustainability issues and considerations into the EU financial services regulatory framework, including the UCITS Directive, the Alternative Investment Fund Managers Directive (AIFMD), MiFID II, the Solvency II Directive, and the Insurance Distribution Directive (IDD).

- The delegated acts also aim to clarify a number of implications resulting from SFDR

- Overview of the proposed requirements:

- MIFID 2 Product governance:

- the delegated act introduces a new definition of sustainability preferences – referring to a client’s or potential client’s choice as to whether a financial instrument that has as its objective sustainable investments, or a financial instrument that promotes environmental or social characteristics as defined in the SFDR should be integrated into their investment strategy

- Investment firms will be obligated to consider client preferences for sustainable products as part of their client’s needs, characteristics and objective as well as whether the relevant product or instrument’s characteristics are in line with the target market, and continues to be so

- MIFID 2 organisational requirements:

- Introduces the definitions of “sustainability preferences”, “sustainability risks” and “sustainability factors”

- Investment firms will be required to consider sustainability risks when establishing, implementing and maintaining risk management procedures which identify the risks relating to the firm’s activities, processes and systems

- Three categories of financial instruments are integral to sustainability preferences:

- Financial instruments that pursue a minimum proportion of sustainable investments in economic activities that qualify as environmentally sustainable under Article 3 of the Taxonomy Regulation;

- Financial instruments that pursue a minimum proportion of sustainable investments, as defined in Article 2, point (17), of the SFDR, where the minimum proportion is determined by the client or potential client; and

- Financial instruments that consider principal adverse impacts on sustainability factors, where elements demonstrate that consideration are determined by the client or potential client

- MIFID 2 Product governance:

- UCITS and AIFMD

- Management companies and alternative investment fund managers (AIFMs) will be required to consider sustainability risks when complying with the organisational requirements and retain the necessary resources and expertise for the effective integration of sustainability risks. In addition, senior management of the management company or AIFM will be responsible for the integration of sustainability risks, and conflicts of interest will need to include those that may arise as a result of sustainability risks.

- Due diligence requirements would also need to include the consideration of sustainability risks

Task Force on Climate-Related Financial Disclosure (TCFD)

The Task Force on Climate -Related Financial Disclosure (TCFD) recommendations are ‘designed to solicit consistent, decision-useful, forward-looking information on the material financial impacts of climate-related risks and opportunities, including those related to the global transition to a lower-carbon economy’.

From 6 April 2022, over 1,300 of the largest UK-registered companies and financial institutions will have to disclose climate-related financial information on a mandatory basis – in line with recommendations from TCFD. This will include many of the UK’s largest traded companies, banks and insurers, as well as private companies with over 500 employees and £500 million in turnover.

Read: Task Force on Climate-related Financial Disclosures Overview pages 4-10

Key points:

- The potential financial implications of climate change include:

- Natural disasters can lead to financial losses (eg infrastructure, cost of rebuilding etc)

- Long-term shifts in the environment and weather patterns could impact the global financial markets

- The process of transitioning to a low-carbon economy can lead to a reduction in the value of certain assets

- Climate related risk can impact credit spreads, influence saving patterns and cause rapid price adjustments

- Climate-related financial risk is non-diversifiable and has the potential to impact company:

- Revenues

- Expenditure

- Assets & liabilities

- Capital & financing

- TCFD was developed by the Financial Stability Board to come up with recommendations for more efficient climate-related disclosures that:

- Could “promote more informed investment, credit, and insurance underwriting decisions”; and

- “enable stakeholders to better understand the concentrations of carbon-related assets in the financial sector and the financial system’s exposures to climate-related risks.”

- Asset owners and managers at the top of the investment chain have an important role to play in influencing the organisations in which they invest to provide better climate-related financial disclosures

- Leaders in the public sector also recognise the importance of transparency on climate-related issues within financial markets

- The Task Force identified several categories of climate-related risks and opportunities:

- Risks

- Transition:

- Policy & legal

- Technology

- Market

- Reputation

- Physical:

- Acute

- Chronic

- Transition:

- Opportunities:

- Resource efficiency

- Energy source

- Products & services

- Markets

- Resilience

- The Task Forces’ recommendations are structured around four thematic areas representing core elements of how organisations operate:

- Governance – Disclose the organisation’s governance around climate-related risks and opportunities.

- Strategy – Disclose the actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy and financial planning where such information is material.

- Risk management – Disclose how the organisation identifies, assesses, and manages climate-related risks.

- Metrics & targets – Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material.

Read: European Securities and Markets Authority- Sustainable Finance Implementation timeline for SFDR, TR, CSRD, MiFID, IDD< UCITS, AIFMD

The graphic shows the timelines for the implementation of sustainability regulation from the EU.

Taskforce on Nature-related Financial Disclosure (TNFD)

Over half of the world’s economic output – circa US$44tn – is moderately or highly dependent on nature.

The TNFD seeks to “develop and deliver a risk management and disclosure framework for organisations to report and act on evolving nature-related risks, with the ultimate aim of supporting a shift in global financial flows away from nature-negative outcomes and toward nature-positive outcomes.”3

In March 2022, TNFD released a beta version of the framework, beginning an 18-month period of consultation and development.

The framework opens with a glossary of key terms to help users understand the framework and the challenges it seeks to address. This includes but is not limited to:

| Biodiversity | The variability among living organisms from all sources, including, inter alia, terrestrial, marine and other aquatic ecosystems and the ecological complexes of which they are part; this includes diversity within species, between species and of ecosystems.4 |

| Cumulative impact | A change in the state of nature (direct or indirect) that occurs due to the interaction of activities of different actors operating in a landscape.5 |

| Dependencies | Aspects of ecosystem services that an organisation or other actor relies on to function. Dependencies include ecosystems’ ability to regulate water flow, water quality, and hazards like fires and floods; provide a suitable habitat for pollinators (who in turn provide a service directly to economies), and sequester carbon (in terrestrial, freshwater and marine realms).6 |

| Dependency pathway | A dependency pathway shows how a particular business activity depends upon specific features of natural capital. It identifies how observed or potential changes in natural capital affect the costs and/or benefits of doing business.7 |

| Direct impacts | A change in the state of nature caused by a business activity with a direct causal link.8 |

| Ecosystem Assets | A form of environmental assets that relate to diverse ecosystems. These are contiguous spaces of a specific ecosystem type characterised by a distinct set of biotic and abiotic components and their interactions.9 |

| Ecosystem Services | The contributions of ecosystems to the benefits that are used in economic and other human activity.10 [i] UN (2021) System of Environmental-Economic Accounting – Ecosystem Accounting |

| Environmental Assets | The naturally occurring living and non-living components of the Earth, together constituting the biophysical environment, which may provide benefits to humanity.11 |

| Impact drivers | A measurable quantity of a natural resource that is used as a natural input to production (e.g. the volume of sand and gravel used in construction) or a measurable non-product output of a business activity (e.g. a kilogram of NOx emissions released into the atmosphere by a manufacturing facility).12 |

| Impact pathway | An impact pathway describes how, as a result of a specific business activity, a particular impact driver results in changes in natural capital, and how these changes in natural capital affect different stakeholders.13 |

| Impacts | Changes in the state of nature, which may result in changes to the capacity of nature to provide social and economic functions. Impacts can be positive or negative. They can be the result of an organisation’s or another party’s actions and can be direct, indirect or cumulative.14 |

| Indirect impact | A change in the state of nature caused by a business activity with an indirect causal link (e.g. a change indirectly caused by climate change, to which an organisation’s greenhouse gas emissions contributed).15 |

| Natural Capital | The stock of renewable and non-renewable natural resources (e.g. plants, animals, air, water, soils, minerals) that combine to yield a flow of benefits to people.16 |

| Natural-climate solutions | A subset of nature-based solutions, natural-climate solutions include conservation, restoration, and improved land and sea management that increase carbon storage and/or avoid greenhouse gas emissions, enhance resilience and assist climate adaptation across global forests, wetlands, mangroves, grasslands, and agricultural lands and other habitats. |

| Nature-based solutions | Actions to protect, sustainably manage and restore natural or modified ecosystems that address societal challenges effectively and adaptively, simultaneously providing human well-being and biodiversity benefits.17 |

| Nature-related opportunities | Activities that create positive outcomes for organisations and nature by avoiding or reducing impact on nature, or contributing to its restoration. Nature-related opportunities can occur i) when organisations mitigate the risk of natural capital and ecosystem services loss and ii) through strategic transformation of business models, products, services and investments that actively work to halt or reverse the loss of nature, including by implementation of nature-based solutions (or support for them through financing or insurance).18 |

| Nature-related risks | Potential threats posed to an organisation linked to its and other organisations’ dependencies on nature and nature impacts. These can derive from physical, transition and systemic risks.19 |

| Systemic risks | Risks arising from the breakdown of the entire system, rather than the failure of individual parts. Characterised by modest tipping points combining indirectly to produce large failures and cascading interactions of physical and transition risks (contagion), as one loss triggers a chain of others and stops systems from recovering their equilibrium after a shock.20 |

| Transition risks | Risks that result from a misalignment between an organisation’s ‘s or investor’s strategy and management and the changing regulatory and policy landscape in which it operates. Developments aimed at halting or reversing the damage to nature, such as government measures, technological breakthroughs, market changes, litigation and changing consumer preferences can all impact risks.21 |

The TNFD draft disclosure recommendations are broken down into four categories: Governance, Strategy, Risk Management and Metrics & Targets.

Governance

- Describe the board’s oversight of nature-related risks and opportunities.

- Describe management’s role in assessing and managing nature-related risk and opportunities.

Strategy

- Describe the nature-related risks and opportunities the organisation has identified over the short, medium and long term.

- Describe the impact of nature-related risks and opportunities on the organisation’s businesses, strategy and financial planning.

- Describe the organisation’s interactions with low integrity ecosystems, high importance ecosystems or areas of water stress.

Risk Management

- Describe the organisation’s processes for identifying and assessing nature-related risks.

- Describe the organisation’s processes for managing nature-related risks.

- Describe how processes for identifying, assessing, and managing nature-related risks are integrated into the organisation’s overall risk management.

Metrics & Targets

- Disclose the metrics used by the organisation to assess material nature-related risks and opportunities in line with its strategy and risk management process.

- Disclose Scope 1, Scope 2, and, if appropriate, Scope 3 greenhouse gas (GHG) emissions, and the related risks.

- Describe the targets used by the organisation to manage nature-related risks and opportunities and performance against targets.

To assist organisations in how to understand and respond to nature-related risks and opportunities TNFD have developed a prototype integrated assessment process for nature-related risk and opportunity management called LEAP:

Locate your interface with nature;

Evaluate your dependencies and impacts;

Assess your risks and opportunities; and

Prepare to respond to nature-related risks and opportunities and report.21

1Lora Froud, T. (2021. Brexit and the Disclosure Regulation. [online] Passle. Available at: <https://blog.macfarlanes.com/post/102gk76/brexit-and-the-disclosure-regulation> [Accessed 17 September 2021].

2Brerly, B. (2022). FCA unveils SDT investment labels. [online] Available at: <https://www.investmentweek.co.uk/news/4058741/fca-unveils-sdr-investment-labels?utm_medium=email&utm_id=be82063416586fbd11bf47d61a4e2664&utm_content=%0A%20%20%20%20%20%20%20%20FCA%20unveils%20SDR%20investment%20labels%0A%20%20%20%20%20%20&utm_campaign=IW%20Daily%2006%20V2&utm_source=IW%20newsletters%20V2&utm_term=CORNERSTONE%20ASSET%20MANAGEMENT> [Accessed 25 October 2022].

3 https://tnfd.global/about/

4 Convention on Biological Diversity (1992) Article 2

5 CDSB (2021) Framework application guidance for biodiversity-related disclosures; Endangered Wildlife Trust (2020) The Biological Diversity Protocol; Capitals Coalition and Cambridge Conservation Initiative (2020) Integrated biodiversity into natural capital assessments; Business and Biodiversity Offset Programme (2012) Glossary

6 SBTN (2022) Working Definitions [unpublished]

7 Capitals Coalition (2016) Natural Capital Protocol

8 CDSB (2021) Framework application guidance for biodiversity-related disclosures; Endangered Wildlife Trust (2020) The Biological Diversity Protocol; Capitals Coalition and Cambridge Conservation Initiative (2020) Integrating biodiversity into natural capital assessments

9 UN (2021) System of Environmental-Economic Accounting – Ecosystem Accounting

10 UN (2021) System of Environmental-Economic Accounting – Ecosystem Accounting

11 UN (2021) System of Environmental-Economic Accounting – Ecosystem Accounting

12 Capitals Coalition (2016) Natural Capital Protocol

13 Capitals Coalition (2016) Natural Capital Protocol

14 SBTN (2022) Working Definitions [unpublished], CDSB (2021) Framework application guidance for biodiversity-related disclosures.

15 CDSB (2021) Framework application guidance for biodiversity-related disclosures; Endangered Wildlife Trust (2020) The Biological Diversity Protocol; ; Capitals Coalition and Cambridge Conservation Initiative (2020) Integrated biodiversity into natural capital assessments

16 Capitals Coalition (2016) Natural Capital Protocol

17 IUCN (2020) The IUCN Global Standard for Nature-based Solutions

18 TNFD (2021) Nature in Scope

19 CDSB (2021) Framework application guidance for biodiversity-related disclosures; TCFD (2017) Final Report: Recommendations on Climate-Related Financial Disclosures

20Goldin, I & Mariathasan, M (2014) The Butterfly Defect: how globalisation creates systemic risks and what to do about it; IRGC (2018) IRGC Guidelines for the Governance of Systemic Risks; Kaufmann, G & Scott, K (2003) What Is Systemic Risk, and Do Bank Regulators Retard or Contribute to It?

21 NGFS (2021) Biodiversity and financial stability: building the case for action

22 https://framework.tnfd.global/the-leap-nature-risk-a